As the dream of homeownership remains steadfast, the traditional path can often present challenges, particularly when it comes to saving for a down payment. In Canada, a rising trend in real estate investing and homeownership is the adoption of rent-to-own (RTO) arrangements.

Spearheaded by property owners and potential buyers, this unique approach offers a symbiotic relationship, allowing tenants to journey towards homeownership while providing landlords with rental income and potential property sales. In this article, we’ll dissect the intricacies of how rent-to-own works in Canada, exploring its benefits, considerations, and the step-by-step process for both parties involved.

What is Rent-to-Own?

Rent-to-own, also known as lease-to-own or a lease option, is a contractual agreement between a property owner (typically a landlord) and a tenant (potential buyer or investor). This agreement allows the tenant to rent the property for a specified period, during which they hold the option to purchase the property at a predetermined price. The option is typically valid for one to three years, providing a defined timeframe for the tenant to decide on homeownership.

Rent-to-Own in Canada: The Process Unveiled

The Rent-to-Own Agreement

The process begins with a comprehensive rent-to-own agreement, a document detailing the terms and conditions of the arrangement. This legally binding contract includes specifics such as the monthly rent, the duration of the option period, the predetermined purchase price, and any potential credits towards the purchase. Clarity and transparency in this agreement lay the foundation for a successful rent-to-own transaction.

Option Fee

To secure the exclusive right to purchase the property at the end of the lease term, tenants typically pay a non-refundable option fee. Distinct from the security deposit and monthly rent, this fee is a critical element of the RTO arrangement, granting tenants the privilege to buy the property during the option period.

Monthly Rent

During the option period, tenants pay a monthly rent, resembling a traditional rental agreement. However, a portion of this rent may be allocated as a rent credit, accruing over time. This credit serves as a financial tool that can be applied towards the property’s purchase price if the tenant decides to exercise their option to buy.

Building Equity

Throughout the option period, tenants have the unique opportunity to build equity in the property through rent credits and potential appreciation in the property’s value. This accumulated equity can be a valuable asset when securing a mortgage for the property purchase.

Property Purchase

As the option period concludes, tenants face a pivotal decision – whether to exercise the option and purchase the property at the predetermined price or let the option expire, allowing the landlord to retain ownership.

How Rent-to-Own Works as an Investment Strategy:

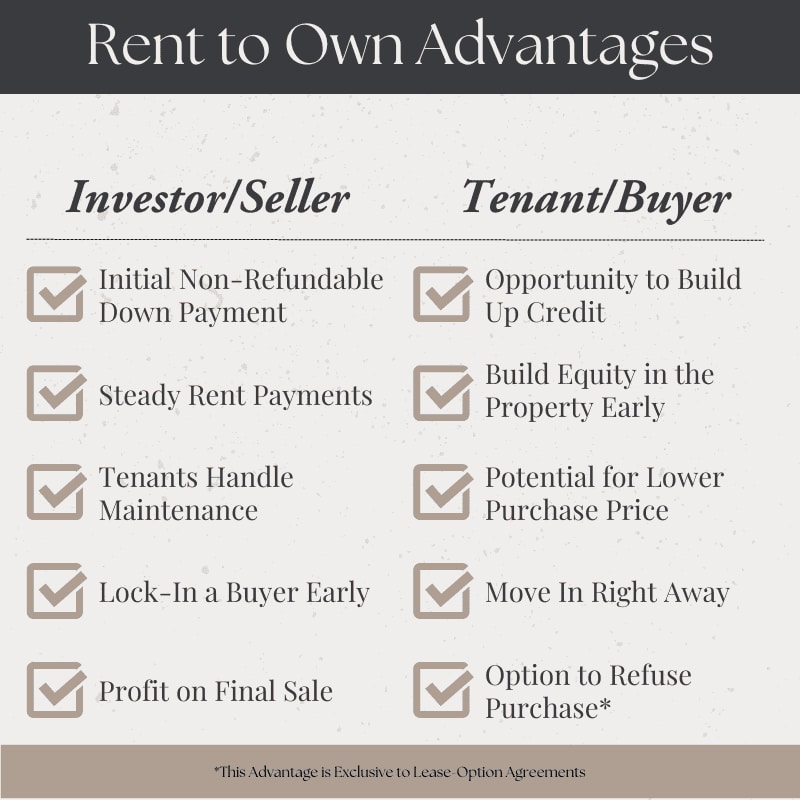

Benefits for Property Owners (Landlords)

- Steady Rental Income: Rent-to-own arrangements offer landlords a stable and predictable monthly rental income. Tenants often pay a premium for the option to buy, resulting in increased rental payments.

- Potential for Higher Selling Price: By fixing the purchase price at the beginning of the option period, landlords stand to benefit if property values rise during the lease term. This could lead to selling the property at a higher price than initially anticipated.

- Reduced Vacancy Risk: Tenants in rent-to-own agreements are more likely to take better care of the property due to their vested interest. This commitment helps reduce the risk of vacancies during the lease term.

- Option Fee: The non-refundable option fee, paid upfront by the tenant, provides an additional income source for landlords. Even if the tenant decides not to purchase, the landlord retains the option fee as compensation for holding the property off the market.

Benefits for Tenants (Potential Buyers)

- Pathway to Homeownership: Rent-to-own arrangements offer a viable route to homeownership for tenants who may not currently qualify for a mortgage. The option period allows them to work on improving credit scores, saving for a down payment, and positioning themselves for future mortgage approval.

- Locking in Purchase Price: Agreeing on the purchase price upfront allows tenants to secure a fixed price for the property, shielding them from potential market fluctuations. This is particularly advantageous if property values are expected to rise during the option period.

- Rent Credit: A portion of the monthly rent, designated as a rent credit, accumulates over the lease term. This credit can be applied towards the property’s purchase price, acting as a valuable contribution to the down payment.

- Test-Drive the Property: Rent-to-own enables tenants to experience living in the property before committing to a purchase. This trial period allows them to evaluate the neighborhood, assess the property’s suitability, and make an informed decision.

Considerations and Challenges of How Rent to Own Works for Property Owners:

- Legal and Regulatory Compliance: Landlords must ensure that rent-to-own arrangements comply with local rental and real estate laws. Seeking legal advice is essential to crafting a contract that adheres to regulations and safeguards the interests of property owners.

- Maintaining the Property: Continued maintenance is crucial for landlords during the option period to uphold the property’s value. Regular repairs and upkeep are necessary to ensure the property remains attractive to tenants and potential buyers.

- Risk of Non-Performance: There’s inherent risk for landlords if tenants choose not to exercise the option to buy. In such cases, landlords must re-market the property to secure a new tenant, potentially leading to lost time and missed investment opportunities.

Considerations and Challenges of How Rent to Own Works for Tenants:

- Non-Refundable Option Fee: The upfront option fee is non-refundable. Tenants must be aware that if they decide not to purchase the property, the option fee will not be refunded, representing a significant financial commitment.

- Financial Responsibility: Tenants bear the financial responsibility for property repairs and maintenance during the option period, simulating the responsibilities of homeownership. This responsibility can be challenging for those not fully prepared for the financial aspects of owning a property.

- Market Risks: If property values decline during the option period, tenants may hesitate to exercise the option to buy, potentially leading to the purchase of the property at a higher price than its current market value.

Conclusion:

In conclusion, understanding how rent-to-own works in Canada unveils a promising investment strategy for both property owners and potential buyers. Landlords can benefit from steady income, potential for increased selling prices, and reduced vacancy risks. Tenants, in turn, gain a pathway to homeownership, the security of a fixed purchase price, and the opportunity to build equity through rent credits.

However, like any real estate investment strategy, rent-to-own comes with its considerations and challenges. Legal compliance, property maintenance, and the risk of non-performance for landlords, along with non-refundable option fees and financial responsibilities for tenants, require careful evaluation.

Approached with transparency, professional advice, and a clear understanding of the terms, rent-to-own stands as a beneficial and rewarding avenue for homeownership and real estate investment in Canada. Both parties should conduct due diligence and assess their financial capabilities and long-term objectives before embarking on this unique and potentially transformative journey.